Proposed Changes to Takeover Code – Presumption of the Definition of “Acting in Concert”

On 26 May 2022, the Takeover Panel (the Panel) published a Public Consultation Paper (PCP) on some proposed amendments to the definition of “acting in concert” under the U.K. Takeover Code (the Code). The presumptions contained in the definition of acting in concert have remained largely unchanged since they were originally introduced, and the purpose of the amendments is to ensure that these reflect changes to the nature of investment markets (since they were introduced) and the current practices of the Panel.

The concept of “acting in concert” refers to persons who, pursuant to an agreement or understanding (whether formal or informal), co-operate to obtain or consolidate control of a company or to frustrate the successful outcome of an offer for a company. Under the Code certain parties are presumed to be “acting in concert” and it is the definitions relating to these presumptions that the amendments address.

Proposed amendments to definition of “acting in concert”

Currently the definition of “acting in concert” under presumption (1) states:

“(1) a company, its parent, subsidiaries and fellow subsidiaries, and their associated companies, and companies of which such companies are associated companies, all with each other (for this purpose ownership or control of 20% or more of the equity share capital of a company is regarded as the test of associated company status)”

The Panel is proposing to amend this presumption and the way in which it operates. In particular, the PCP proposes to change the presumption in the following principal ways:

- Raise the threshold in the current presumption (1) for the definition of “acting in concert” in the Code from 20% to 30%, to align it with the threshold for the Code’s definition of “control”.

- The voting rights and equity share capital and the dilution of interests held through chains of ownership are to be clarified for the purposes of determining parties that are acting in control through connected companies.

- A new presumption (New Presumption 1) will be introduced whereby a company (Company X) and any company which controls, is controlled by or under the same control as Company X, are all presumed to be acting in concert with each other. “Control” here would be defined as where a company is interested in either shares carrying 30% or more of the voting rights in a company or a majority (more than 50%) of the equity share capital in a company.

- An additional presumption (New Presumption 2) will be introduced whereby the following companies will all be presumed to be acting in concert with each other: a company (Company Y) and any other company (Company Z) where Company Y is interested, directly or indirectly, in 30% or more of the equity share capital in Company Z, together with any company presumed to be acting in concert with either Company Y or Company Z under New Presumption 1.

The presumptions will apply to interests both to shares carrying voting rights (whether or not the shares are also equity share capital) and equity share capital (whether or not the shares also carry voting rights). However, both New Presumption 1 and New Presumption 2 will apply to funds in the same way as to companies, thereby, in effect, treating an investment in a fund as equivalent to an investment in a company’s equity share capital. Where a fund is managed by an independent discretionary fund manager, the fund manager (but not the investors in the fund) will, in general, be interested in any securities held by the fund by adding a further new presumption.

Example of application of New Presumption 1

In practice the effect of New Presumption 1 would mean that companies that are connected by 30% or more of the voting rights or more than 50% of the equity share capital would be considered to be “acting in concert”. Furthermore, under the New Presumption 1, percentage interests would not be diluted through a chain of ownership.

What this means is that, if there are three companies A, B and C, where A owns or controls 30% or more of the shares with voting rights attached in company B, and B owns or controls 30% or more of the shares with voting rights attached in Company C, then companies A, B and C will be considered to be acting in concert with each other, irrespective of whether A owns or controls any equity share capital in B and whether or not B owns or controls any equity share capital in C.

The Panel explains the reasoning for this being that, in these circumstances A will be treated as controlling B, which in turn is treated as controlling C as shown in Diagram 1 below:

Diagram 1: Companies A, B and C would all be presumed to be “acting in concert”

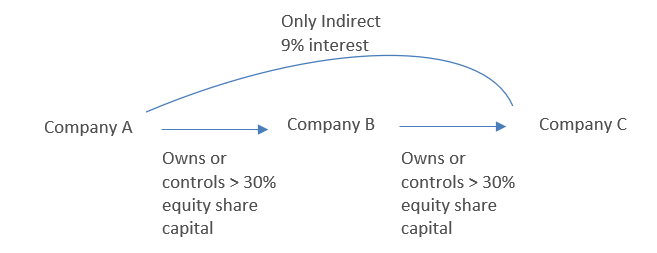

Example of the application of New Presumption 2

In practice, the effect of New Presumption 2 would be that, if there are two companies connected by 30% or more of the equity share capital (including voting and non-voting rights attached) and there is a third company which, under New Presumption 1, is already presumed to be “acting in concert” with either of the former two companies, then all three companies will be presumed to be “acting in concert”. However, under the New Presumption 2, the percentage interests would be diluted through a chain of ownership.

What this means is that, if there are three companies A, B and C, where A owns or controls 30% or more of the equity share capital of B and B owns or controls 30% or more of the equity share capital of C, then A and B, and B and C, are separately presumed to be acting concert with each other, but A and C would not be presumed to be acting in concert with each other.

This is because company A is indirectly interested in only 9% of company C’s equity share capital as shown in Diagram 2 below. The Panel’s logic for this is that A and C would be unlikely to be incentivised to take action to support each other.

Diagram 2: Companies A and C not presumed to be “acting in concert”

What other scenarios might be considered to be acting in concert?

The above examples represent the most basic examples provided by the Panel in the PCP. With there being various ways that companies might own shares/share capital in other companies, there are numerous scenarios in which complex corporate arrangements may or may not mean companies are acting in concert under these new presumptions, requiring an analysis of corporate structures and shareholdings.

In the PCP, the Panel set outs a non-exhaustive list of example scenarios where companies may or may not be acting in concert with each other. This obviously cannot cover every conceivable situation that may occur but provides a point of reference for advisors to consider when discussing concert party issues.

The Panel has at this time provided no guidance to how these new presumptions will interact with wholly owned government entities, but has suggested they anticipate providing general advice on this point in the near future as a part of any Response Statement.

Timing

The consultation period proposed by Panel ends on 23 September 2022, and they anticipate providing a Response Statement in late 2022 and expect that the amendments to the Code would come into effect approximately two months after the publication of the Response Statement.

How can Armstrong Teasdale help

Armstrong Teasdale is well versed in guiding and assisting clients through Takeover Code-related issues that arise in the course of transactions. If you have any queries regarding the Code in relation to a potential transaction, please get in touch with us to discuss things further.

Disclaimer: This publication is provided by Armstrong Teasdale Limited for informational purposes only. The information contained in this publication should not be construed as legal advice. Any questions or further information regarding the matters discussed in this publication can be directed to Armstrong Teasdale’s U.K. Capital Markets team.